CLEVELAND, OH – Quicken Loans (also dba as Rocket Mortgages and Rocket Companies) discriminates against Protestant Christians, Catholics, Muslims, Buddhists any every other borrower who isn’t a Jew; and who Dan Gilbert’s redlining corporation has foreclosed on for non-payment of mortgages despite all the “interest” a buyer has earned from their home purchase investment. The discrimination comes in the form of his agreeing to an Israeli rabbinical court in America’s ruling that one Jew can’t charge another Jew interest on a loan. It’s in their “mitzvots.”

Gilbert disavowed federal mortgage and discrimination laws enacted by the United States Congress when he entered a “liturgical agreement” based on the April 23, 2018 rabbinical court “ruling of the Conference of the Synagogue Rabbonim of Agudath Israel. These individuals are Ashkenazi and Haredi Jewish rabbis who make up the Rabbonim of Agudath Israel. Rabbonim is another word for “rabbi.”

The liturgical agreement was enacted with a “council of Torah sages.” The wording of the liturgical ruling from the Jewish rabbinical court that led to the liturgical agreement is as follows:

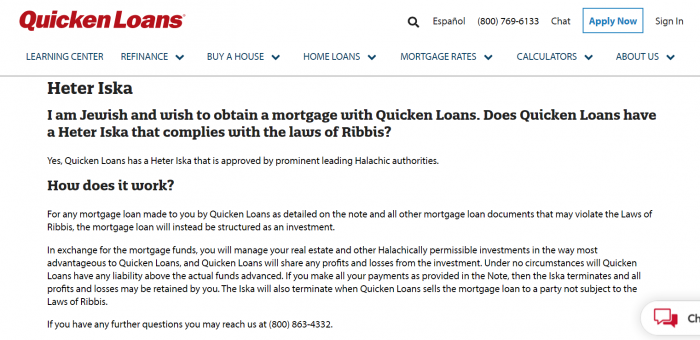

Quicken Loans (QL), a leading mortgage lending institution in the USA, is Halachically under majority Jewish ownership. Upon thorough investigation, prominent leading Halachic authorities have issued a P’sak [click here for link] that any Jew who obtains a loan with interest from QL or any of its subsidiaries [i.e. Rocket Mortgage] is in danger of transgressing the prohibition of Ribbis D’oraisa.

It has come to our attention that upon inquiry from prospective customers, QL has been providing information stating that there is no need for a Heter Iska when obtaining a mortgage from them. We therefore feel compelled to counter this misinformation by alerting the public to the P’sak of Gedolei HaRabbonim which states unequivocally that it is forbidden Al-Pi Torah for any Jew to take a mortgage or any other form of loan from Quicken Loans or its subsidiaries – or any other Jewish-owned lending institution – without a valid Heter Iska.

According to the group of ultra Orthodox Jewish rabbis coordinating religious edicts between Europe, North America and Israel, if Gilbert wants Jewish business it has to be transacted with a heter iska when the financial institution organized under federal laws is “halachically under majority Jewish ownership.” Pursuant to Jewish law found in the Torah, anyone who practices another religion to follow God is a “non-believer” or “goyim.” We’re pagans so it’s okay to charge “us” interest with a guilt-free conscience according to Agudath Israel spokesman Rabbi Chaim Jachter.

Jachter’s instructional words to Jews are reflected below in a piece the allegedly Godly man wrote captioned: “Halachic Status of a Corporation, Part One: Introduction to Ribbit and Heter Iska.” His thinking is insidiously Satanic.

We began by noting that the Torah (Devarim 23:20-21) prohibits Ribbit between Jews. However, it does permit Ribbit when lending to a non-Jew. We noted an explanation I heard long ago from Rav Yehuda Amital, the founding Rosh Yeshiva of Yeshivat Har Etzion.

There is nothing morally wrong with charging a reasonable rate of interest. After all, the financial role or function of wealth is to generate more wealth. When one lends money his wealth is held dormant and is not able to create further wealth. The borrower, on the other hand, is able to use the money to make more money. Why, then, should not the lender be morally entitled to a reasonable rate for allowing his counterpart the potential to generate wealth?

However, we fellow Jews are brothers, as the Torah explicitly states in this context. One acts differently with family than with those outside one’s family. For example, one would happily host a family member for months on end if necessary, whereas he would not necessarily do this for someone outside his family.

Similarly, we are expected to extend interest free loans to our fellow Jews in need. Indeed, Hebrew free loan societies have existed on every Jewish community worthy of being called a Jewish community in every generation. This is part of the familial responsibility we have towards each other.

Of course, the Gemara (Gittin 61a) instructs us to support non-Jewish poor along with the Jewish poor. However, the scope of the responsibility we have towards our Jewish family members extends beyond that which applies to those who are not part of the family.

Most interestingly, the prohibition to lend money to a Jew with interest does not apply to non-observant Jews according to many Rishonim (see Tur and Shulchan Aruch Yoreh Dei’ah 159). According to this approach, the Ribbit prohibition is a means by which we foster a sense of brotherhood amongst our fellow Torah observers. It is a way through which we help each other live a Torah life. Thus, someone who is not part of the brotherhood of Torah observers might not be due the benefit of having an interest free extended to him. It should be noted that this view was not accepted by Rashi, and Rama recommends that no interest should be charged to non-observant Jews.

Ribbit translates to “compensation.” The word “halachic” simply translates to “Jewish law.” The rabbinical judges are called “sanhedrin.” Behind all the combinations of Yiddish and Hebrew words is nothing more than Gilbert turning Quicken Loans and Rocket Mortgage into a Racketeering Influenced Corruption Organization (RICO) controlled by racist Jewish supremacists.

The “Gemara (Gittin 61a)” Jachter wrote of above interprets to the following: “Everyone agrees that since they are receptacles that hold the fish or animal entering them, by right the trapped animals belong to the owner of the trap. When they disagree, it is with regard to a fishhook or other traps [kokrei] that merely catch the fish or animal but are not receptacles that hold it. In such cases, there is reason to say that the owner of the trap does not take possession of the trapped animal, and therefore another person who takes it is guilty only of robbery on account of the ways of peace.“

The bottom line to this discussion is that Gilbert’s goyim customers are the one’s paying interest and losing their homes, businesses and possessions for non-payment. He’s letting God’s chosen people from Russia, Poland and the Ukrainian live financially stress-free lives. None of the pagan names quoted in the Bible to describe Jews have origins to Russian, Poland and the Ukraine or anywhere else in Eastern Europe. Christians and Muslims are semitic people and the United States of America is a majority semitic nation of Christians.

The result of Gilbert‘s special Jewish only “heter iska” is Jews get a check instead of court-ordered foreclosure eviction notices for non-payment of what for every other one of his Christian and Muslim borrowers is a “mortgage.” Since Redlining Gilbert sells off his loans, if the owners of the equity firms buying the notes he’s sold are Jews, the heter iska is still a Jew-only deal and enforceable. If goyim or Protestant and Catholic Christians own the financial institution the heter iska is null and void; and Jews are treated like every other borrower.

There is only one set of federal mortgage laws under the banking section of Title 46 of the United States Code. Terms like “mortgages” are defined as well as “discrimination” along “religious” lines. Quicken Loans will face tremendous “class action” pressure from Protestant and Catholic Christians who comprise the nation’s overwhelming majority of borrowers he’s discriminating against as word of his Jewish supremacist deal spreads. The United States of America is not nor will it ever be Palestine; and Americans aren’t going to be “knowingly” treated like Palestinians by a 1.6 percent minority.

No federal law includes the use of the Russian Jewish term “heter iska” as a legal instrument for buying a home that turns the mortgage into an “interest free investment” that doesn’t come with foreclosure for non-payment. There’s also no reference to “liturgical agreements” I’ve found on the Supreme Court of the United States’ website. I didn’t search Lexis Nexis.

These terms and practices are as fundamentally un-American, unlawful and invalid as the subpoenas sovereign citizens are issuing. If Gilbert was loyal to America he would have seen and called out the scheme’s inherent law breaking racism.

I reviewed Gilbert’s “Rocket Companies” Annual 10k filing with the Securities & Exchange Commission (SEC) for the period ending December 31, 2020. It “appears” as if he’s hiding the discriminatory practice by describing it as a “personal loan.”

While the characteristics of all loans are the same, the language used by Gilbert’s 10k report writers sounds like the type of cases being resolved by the rabbinical courts like Beth Den. The words “heter iska” don’t appear in Rocket Mortgages initial filings to the SEC in 2020.

Our personal loans are not secured, guaranteed or insured and involve a high degree of financial risk.

Personal loans made through our Rocket Loans platform are not secured by any collateral, not guaranteed or insured by any third party and not backed by any governmental authority in any way. We are therefore limited in our ability to collect on these loans if a client is unwilling or unable to repay them. A client’s ability to repay their loans can be negatively impacted by increases in their payment obligations to other lenders under mortgage, credit card and other loans resulting from increases in base lending rates or structured increases in payment obligations. If a client defaults on a loan, we may be unsuccessful in our efforts to collect the amount of the loan. As such, our partner bank Cross River Bank could decide to originate fewer loans on our platform and there could be less demand in the secondary market for loans originated through the RocketLoans.com site.

Huntington Bank’s chairman, Gary Torgow, in 2018 had these words to say about Gilbert’s Jewish supremacy. “Dan Gilbert and his team at Quicken Loans wonderfully demonstrated deep sensitivity to the concerns of Jews around the world with his decisive action on this issue. I’m extremely gratified that Dan’s determination to do what needed to be done will benefit so many members of the Jewish faith.”

Torgow was the president of Michigan’s Chemical Bank at the time. There’s no record of the board implementing a heter iska there or at Huntington. The fact that Torgow thinks this Jewish supremacist practice is blendable with our laws in the United States of America makes both him and Gilbert a threat to the economic interests of every Christian and non-Jew in our nation.

From an American perspective Agudath Israel was organized in Katowce, Poland in 1912 and in the United States of America in 1922. When the illegal Russian, Polish and Ukrainian alien immigrants to Palestine armed themselves to take over and set up their own government in 1948, with $50 million in funding from illegal Russian, Polish and Ukrainian aliens in the United States of America, their rabbinical courts were aligned and coordinated within the new Government of Israel through a modus vivendi. There’s an Agudath Israel office in South Euclid on Warrensville Center Road.

In diplomacy the term modus vivendi means “way of life.” None of Agudath Israel’s espionage-related acts and private agreements between foreign interests were revealed to or approved by either the United States Department of Justice or the United States Department of State; and Jewish politicians benefitting from the heter iskas know this preferential treatment exists in contradiction to federal and state laws. The “interest free” loans their families have benefitted from since 1948 have never been investigated by Congress.

Were the 3rd party tax lien sales James Rokakis asked the General Assembly of Ohio to enact in 1998 a seed planted that would lead to a foreclosure crisis in Cuyahoga County which has displaced over 100,000 homeowners whose properties were foreclosed on and possibly purchased by Jews with interest free loans? With Russian, Polish and Ukrainian Jews controlling the majority of northeast Ohio’s lending institutions are the “heter iskas” the reasons majority Jewish populated or politically controlled cities like Cleveland Heights, Beachwood, South Euclid, Shaker Heights, Woodmere, Orange, Pepper Pike, Solon and Hudson have so many more businesses and owned homes?

Joel Ratner was accused of being a racist by former Ward 4 Councilman Kenneth Johnson for distributing more than $6.5 million in neighborhood development funds to the west side from his east side headquarters at St. Luke’s old hospital site. $1.5 million was invested by Neighborhood Progress on the east side. The psak from the rabbinical court raises the thought that every “spending” board or commission that is majority controlled by Jews should be investigated to learn if they’re using the bodies to enrich other Jews instead of a fund’s intended recipients.

The Conference of the Synagogue Rabbonim of Agudath Israel is a Hebrew court operating inside the United States of America, but under the direction of the same court organized by the Government of Israel. To the Zionist Jews in 1926, Agudath Israel was called a “menace to Jewish unity” by the World Zionist Council (WZC). Like the WZC and AIPAC, Agudath Israel has failed to register as Israeli agents under the Foreign Agents Registration Act (FARA) for being “directed” by Israeli government officials to conduct “missions” inside the United States of America.

The pressure campaign on Gilbert was a mission and he bowed to then Prime Minister Benjamin Netanyahu’s covert demands through the rabbinical court. The Agudath Ysreal of Israel is firmly behind the Hiter-like Netanyahu. When Gilbert issued the following statement he was disavowing American laws. He was following Netanyahu’s orders to establish a separate Zionist “way of life” as it pertains globally to borrowing, credit and interest transactions involving Jews.

“Over the next 30 days, Quicken Loans will assemble a committee to quickly and efficiently dive into the issue of ‘Heter Iska,’ and once and for all attempt to find a solution that the observant Jewish community, as well as our legal and capital markets team, finds acceptable. I am confident that this can and will be achieved.”

President Harry Truman’s administration directed the WZC to register as foreign agents in 1948. Shaker Heights resident Isaiah Kenen changed the name of his group to the American Israeli Public Affairs Committee (AIPAC) to obstruct our government’s enforcement of espionage laws. Zionist Kenen in 1926 from his home at 17412 Winslow Road in Shaker Heights had these words to say about the Agudath Israel Jews who directed Gilbert.

“The Agudath Israel is trying in every possible way to undermine not only the Zionist Organization, not only Jewish national sentiment but every effort at a united front among the Jewish people. Their policy is ‘divide and rule.’ In Poland as in Palestine, in Austria as in Czecho-Slovakia, they seek to make impossible the creation of a united Jewish front.

“In Poland the Jews succeeded in electing several of their own members to the Polish Parliament, but the Agudath Israel deputies refused to join the Jewish Political Club to which all the other deputies, from Right to Left belonged. Only the anti-nationalist Jewish Socialist members of Parliament remained outside of the Club and their only political allies were the representatives of the Agudath Israel.

“In Czecho-Slovakia there was attempted a creation of a unified Jewish election bloc, but the Agudath Israel forces were the only ones who prevented the realization of these aims. Thanks to their efforts not a single Jew was elected.

“But the activity of the Agudath Israel in Palestine is even more disgraceful. Until the close of the war, the rebuilding of Palestine was not part of their program. They even reproached the Mizrachi for giving so much attention to Palestine in comparison with the Golus at a time when there were very few Jews in the Holy Land. It was only after the war that the Agudath realized that it was possible to make trouble even in Palestine, and since the Agudah is ‘active’ in Palestine, the full effect of its work is felt whenever there is about to be unity in Jewish work.

Americans invested in the United States Constitution, federal laws and codes should imagine a religious court deciding all matters of civil and criminal disputes between Jews inside our nation that may even come with Old Testament death penalty offenses. Every other citizen of the United States of America lives with federal banking, mortgage, lending and Security & Exchange Commission laws now overseen by 33 Russian Jewish members of a 435 member Congress.

Four Jews serve on our nation’s 12 member Supreme Court. Now imagine them voting and ruling on federal financial laws they know they’ll leave their Congressional offices after work and join with other members of their faith to ignore. It would be of interest to study how elected and appointed Jewish judges have been deciding the fate of financial transactions in disputes between Jews and Christians.