CLEVELAND, OH – In addition to my career as an investigative journalist, I am a former mayor, a United States Air Force veteran, and until recently, a USAA policyholder who trusted the company to treat me fairly after a minor collision. What I discovered instead is a systemic pattern of deception involving artificial intelligence, vendor harassment, and regulatory evasion that should alarm every insured driver in America. I learned of possible violations involving CCC ONE and CCC Intelligent Solutions that are reportable to the Securities & Exchange Commission (SEC) and the Ohio Department of Insurance.

The focus of my concern is how USAA and its Artificial Intelligence (AI) vendor CCC Intelligent Solutions (NASDAQ: CCCS) are using the flawed algorithms and incomplete prompts of its CCC ONE program to systematically undervalue vehicles, and how two employees of USAA vendors I spoke to inside the system confirmed the inaccuracies.

On January 29, 2026, another motorist struck the passenger side of my 2014 Jeep Grand Cherokee Limited. It was a low-impact collision that resulted in two doors being scraped, minor wheel well dents, nothing catastrophic. The two doors and wheel wells cost less than $2000 from a wrecking yard. I filed a claim with USAA and scheduled a February 17, 2026, appointment with their approved repair specialist, Caliber Collision in Bedford Heights, Ohio.

My Jeep is not an ordinary 2014 model. While the chassis is 12 years old, under the hood sits a 2020 replacement engine with between 60,000 and 70,000 miles on it. The original engine was replaced in 2023 after a prior owner had a parking lot collision and it sat for two years.

I purchased the vehicle from a Cleveland body and mechanic’s shop owned by brothers Rob and Ken Tate in July 2023 and have put about 33,000 miles on it since. The engine has about 60,000 – 70,000 total miles — not the 181,551 showing on the odometer. The 2020 Jeep engine was installed with about 34,000 miles on it.

My 2014 Jeep Grand Cherokee Limited was also customized with a 2020 grille and a black Hemi hood. The vehicle is, in essence, a 2014 chassis with a 2020 heart and look. None of that would matter to an artificial intelligence algorithm.

On February 18, 2026, a Caliber Collision appraiser prepared two documents for my claim. The first was a repair estimate in Caliber Collision’s system. It was detailed and professional. Lines 21 and 22 show $218.95 to replace the locked passenger side seat belt — a critical safety defect I had pointed out to the appraiser in person when I delivered the vehicle for repair estimate. We had also discussed the engine and body modifications.

The second document was a valuation report generated by CCC ONE, the artificial intelligence platform owned by CCC Intelligent Solutions and used by USAA’s adjusters to value my vehicle and compare it to the cost of repairs. This report would determine whether my vehicle was repairable or a total loss.

Page 8 of the CCC ONE report contains no mention of any seat belt. Not in Interior. Not in Mechanical. Not anywhere. It looked like the same appraiser, on the same day, documented the truth in one system and hid it from the other, but that’s not what happened.

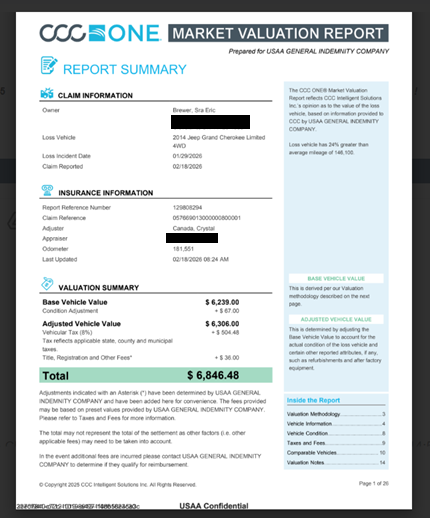

The CCC ONE report also completely ignored the 2020 engine. Page 5’s “Engine” field is blank. Page 16 of the same CCC ONE report contains AutoCheck records showing the engine was serviced in May 2021 at 147,820 miles. The report USAA was using from CCC ONE had the data that my Jeep had an engine. The algorithm ignored the fact my Jeep had an engine.

The result? CCC ONE valued my entire vehicle at $6,239 — about $6,000 less than its actual cash value, and barely more than the $5,800 repair estimate from USAA’s own collision center. My comparable showed it costing between $10,000 and $13,000 to replace a Jeep with between 180,000 and 210,000 miles.

What USAA Didn’t Tell Me

USAA sent me a total loss settlement letter right after I received my estimate from Caliber Collision. They weren’t going to repair my vehicle. They were offering me a settlement of $6239 to buy another vehicle. I had to sign over my title and let them sell it through their vendor, CoPart, for scrap.

If I wanted to keep the vehicle, USAA’s adjuster offered to deduct $1900 from the amount they would sell it to CoPart for and give me $4339 for another vehicle. That’s about the cost of repairs I obtained from an appraiser not connected to USAA. Of course, my clean title would be slandered as salvage. I rejected the offer and called Caliber Collision to let them know I was retrieving my car. The deal they offered was stupid.

I informed USAA I was exercising my option to obtain an independent estimate.

Under Ohio law, and in my opinion, the scheme they outlined to obtain my Jeep is conversion — the wrongful exercise of dominion over property belonging to another. USAA has no ownership interest in my vehicle. I never signed over my title. I have never agreed to a total loss settlement.

Nothing about my interaction with USAA and its vendor made sense, so I decided to investigate. I read the entire CCC ONE loss report and started investigating the company.

I learned CCC ONE was an artificial intelligence tool. The company itself describes its products as “AI-powered systems” and “cloud-based software solutions.” That had not been disclosed to me by USAA. No adjuster or supervisor told me verbally or in writing that CCC ONE’s loss was based on an artificial intelligence analysis.

USAA had described CCC ONE as a “state approved method.” The deceptive wording suggested that the San Antonio, Texas headquartered insurer’s use of artificial intelligence to appraise vehicles was “codified” by the General Assembly of Ohio in the Ohio Revised Code, so I checked. There are no Ohio laws that allow for artificial intelligence generated insurance loss appraisals.

According to the CCC ONE total loss report from USAA’s adjuster, the AI tool locates similar vehicles, adjusts for differences, averages the values, accounts for condition and refurbishments. The CCC ONE loss report contained this promise: “If you find USAA has missed an option or you find a discrepancy, your CCC ONE Market Valuation Report can be updated; however, proof of the discrepancy must be provided.”

The proof my Jeep was equipped with an engine was in the Caliber Collision estimate and not in the CCC ONE total loss report, an obvious discrepancy that should have generated questions from USAA’s adjusters. As my knowledge grew so did my resistance to USAA’s legally unsupported tactics.

When I pointed out the discrepancies in the CCC ONE report to USAA adjuster Giovanna Cardenas, she responded for the company that it was sticking with the report. She told me her supervisor would not override her decision and he didn’t. She suggested that I show proof of purchasing and installing a 2020 engine in a 2014 Jeep Grand Cherokee Limited.

My response was USAA should have instructed Collision Caliber to check my engine block for the Engine Identification Number (EIN) for the manufacture date. Had a human instead of an AI tool appraised my vehicle that would have been an easy fact to verify.

It is ridiculous I have to pay for a human to appraise my vehicle when the humans USAA directed me to for an appraisal had the vehicle in their possession and the tools to confirm its existence and manufacture date. USAA’s approved AI tool did not have the correct field to identify it. Bad faith.

The whistleblowers speak

In the course of fighting this claim, I spoke directly with two people inside the system. Their admissions are devastating, so I’m not adding pressure to their lives by publicly naming them. Should the Ohio Department of Insurance under former Supreme Court Justice Judith French launch an investigation their testimony is up close, detailed and important.

The appraiser who prepared both documents, confirmed that she saw and acknowledged the 2020 engine and discussed it with five officials. In the end she was instructed to leave it blank because CCC ONE “didn’t have a field for it.” When asked about CCC ONE’s accuracy, her assessment was critical. It’s a defective tool.

Before I could retrieve my vehicle, I started receiving text messages and calls from employees of CoParts, another USAA vendor, seeking to schedule my Jeep for pickup. This was after I told USAA no deal and I told CoParts’ employees not to contact me anymore. They didn’t stop. Its most recent contact was March 4, 2026, while USAA agents know I’ve exercised my right to an independent appraisal and have been clear I am not scrapping my vehicle.

When I spoke to the CoPart employee who called me on March 4, 2026, to schedule my Jeep for a pickup, she shared that Copart’s contract with USAA requires daily calls to claimants, regardless of whether the claim is resolved or in dispute. She had forwarded seven communications to USAA documenting my repeated verbal and written instructions to stop calling, and USAA had not responded back. In compliance with their agreement, she said, they had no choice but to continue the calls and texts until they heard from USAA.

“This is harassment,” I told her. She didn’t disagree and said she would advise CoPart officials not to call anymore. The USAA vendor’s employee said she has to “fix” bad data all the time because of the inaccurate information generated by CCC ONE. When I asked about her experiences with CCC ONE. Her response was terse. “Not good.”

The Algorithm’s Design: Built to Manufacture Total Losses

What I’ve learned since my accident and investigation is that CCC ONE is not just accidentally inaccurate. It is architecturally designed to prioritize speed over accuracy.

Adjusters at companies like USAA are measured by KPIs (Key Performance Indicators). The most weighted KPI is almost always Cycle Time or the number of days from “First Notice of Loss” to “Settlement.” It’s standard industry operating procedure.

When a USAA adjuster is at their computer inputting data for a vehicle valuation in CCC ONE, they encounter a series of screens. Contacts, Vehicle, Options, Condition, Refurbishments. The “Refurbishments” page contains fields for items like “Rebuilt/Replacement Engine.” But entering information in these fields triggers a “manual review” that adds 24–48 hours to the claim and slows down the process.

Since adjusters are graded on “cycle time” or how quickly they close claims, supervisors may instruct them to leave the refurbishment fields blank to prevent their metrics from declining. By being honest and treated trusting veterans fairly, they get penalized.

While USAA and CCC ONE may claim to value accuracy, worker performance is often measured by “Internal Audits.” If the AI (CCC ONE) says $6,239 and the adjuster accepts it, the “Audit” shows 100 percent alignment. If the adjuster changes the number, it triggers a “Variance Report,” which looks bad on their scorecard.

In 2026, many remote adjusters are monitored by “Time-on-Task” software. If a remote working adjuster stays on the “Refurbishments” screen too long without clicking “Next,” the system might flag them. It’s a work reality that creates a high-pressure “Assembly Line” environment.

The bottom line is USAA’s KPIs are in direct conflict with their “Duty of Good Faith.” Pursuant to Ohio Administrative Code section 3901-1-54, an insurer must conduct a “reasonable investigation” in determining loss. If USAA’s internal KPIs penalize an adjuster for doing a “reasonable investigation,” then the company is essentially mandating bad faith through their performance metrics.

One of the additional flaws in the system is that the valuation module doesn’t ask “Is the seat belt broken?” It presents broad categories such as Engine, Transmission, Interior, Dashboard that are rated by an agent clicking one of four buttons. Below Average, Average, Above Average, Exceptional.

A locked seat belt, a critical safety defect, gets “averaged out” by the “GOOD” rating for seats and carpet. The system is designed to launder specific defects into vague categories that suppress value. CCC ONE doesn’t care about USAA’s veteran’s customers safety.

The estimating module (used by Caliber) connects to parts databases and captures specific defects like a $128 seat belt. The valuation module (used by CCC ONE) connects to market databases and uses broad condition categories. The two systems do not talk to each other.

The Regulatory Framework USAA Is Violating

In December 2023, the National Association of Insurance Commissioners (NAIC) adopted a Model Bulletin on the Use of Artificial Intelligence Systems by Insurers. Ohio has adopted these standards, and Ohio Department of Insurance Director French holds leadership roles within the NAIC, which has made “AI Model Governance” a 2026 priority.

The bulletin requires insurers to identify AI systems used in decisions affecting consumers, maintain a written AIS Program governing AI use, ensure human oversight of algorithmic decisions, guarantee transparency and explainability of outcomes, monitor for model drift and accuracy decay, control third-party AI vendors through contracts and audits.

On February 27, 2026, just last week, Ohio Department of Insurance Director French was announced as the chairperson of NAIC’s Innovation, Cybersecurity, and Technology Committee as well as co-chair of the Risk-Based Capital Model Governance Task Force. They’re supposed to be working to “strengthen the U.S. state-based system of insurance company financial regulation and solvency oversight.”

I will file a formal complaint with the Ohio Department of Insurance requesting a Market Conduct Examination into USAA’s use of CCC ONE. An independent appraiser will conduct a “Critical Study” of my vehicle. Personally, and politically, I think Ohio voters should enact a constitutional amendment banning artificial intelligence in the insurance appraisal and rating process. It’s not fair to the trusting insurance customer.

I sent USAA 24 questions I want them to answer. If they answer truthfully, they admit they’re screwing over U.S. armed forces veterans and their family members. If they answer evasively, they provide evidence of bad faith. If they refuse to answer, they confirm they cannot defend their conduct.

If you are reading about my interaction with USAA and wondering whether the same thing could happen to you, the answer is yes. It can. It will. It already has and you don’t know. It is happening to tens of thousands of Americans right now, quietly without anyone noticing. Artificial intelligence is also being forced down your throats by states that mandate its residents to purchase automobile insurance instead of creating heavily codified, state-run shared risk insurer pools. Insurers are seeking government sanctioning for a tool whose programming they control to take more money from its customers to keep in their pockets.

Here is what you can do:

Know your vehicle. Document every modification, every repair, every refurbishment. Keep records. Take photos. If you have a newer engine, get an ECU scan to prove its actual mileage.

Challenge the algorithm. When an insurer sends you a CCC ONE report, read it. Compare it to your records. If something is missing, document it in writing. Use the language of the regulations. Cite OAC 3901-1-54. Make them respond.

Demand a physical inspection. If the appraiser never touched your vehicle, demand to know why in writing. A locked seat belt cannot be seen in photographs. A replacement engine cannot be verified without opening the hood. A new transmission

Watch NMVTIS. If your vehicle is declared a total loss, check whether it has been reported to the National Motor Vehicle Title Information System. If the report is inaccurate, demand its correction. A false salvage brand can follow your vehicle forever.

Share your story. The only thing more powerful than an algorithm is public awareness. If this happened to you, tell someone. Write to your legislator. Contact the Ohio Department of Insurance. Make your voice heard.

This is not about the money. It is about the principle. I am offended that an insurer’s use of artificial intelligence appears rigged to strip me of my property rights without ever laying eyes on what it is destroying.

My car still drives perfectly. The engine purrs. The steering is firm. The suspension system handles all terrains well.

It’s a good car. Paid for. I’m an elderly veteran, 72, living on a fixed income. I don’t have a need to drive every day, and I planned to keep my Jeep until the end.

As a teenager my first real job was for a Phillips 66 filling station in East Saint Louis, Illinois in 1967. I pumped gas. Today, only two states still require someone to pump your gas for you. Technology took those jobs, just as algorithms are now taking human judgment from insurance claims

I want a human involved in every aspect of a vehicle that can protect or threaten my life and the lives of others. The human appraisers I interacted were being treated as subordinate to Artificial Intelligence instead of its masters.

The concept of any human’s thinking being made subordinate to the reasoning of artificial intelligence is an absurdity Americans and Ohioans should not tolerate.

hello world

hello world

vardenafil price

vardenafil price

mobic 7.5 mg oral tablet

mobic 7.5 mg oral tablet

what is zoloft

what is zoloft

avanafil stendra buy

avanafil stendra buy

lasix furosemide 40 mg

lasix furosemide 40 mg

fluconazole 100 mg

fluconazole 100 mg

cenforce 50 vs viagra

cenforce 50 vs viagra

tadalafil hersteller unterschiede

tadalafil hersteller unterschiede

creon medicine generic

creon medicine generic

semaglutid spritze hersteller

semaglutid spritze hersteller

levitra indian brand

levitra indian brand

doxycycline for uti in cats

doxycycline for uti in cats

doxycycline 100mg for women

doxycycline 100mg for women

bupropion xl 150 reviews

bupropion xl 150 reviews

ketoconazole information

ketoconazole information

toradol pharmacology

toradol pharmacology

ketorolac tromethamine

ketorolac tromethamine

toradol migraine overview

toradol migraine overview

minoxidil medical reference

minoxidil medical reference

ED medication high‑fat meal delay

ED medication high‑fat meal delay

orlistat food interaction evidence

orlistat food interaction evidence